RBI MPC June 2026: Repo Rate Held at 5.25% — What It Means for You

RBI MPC kept the repo rate unchanged at 5.25% in June 2026 amid geopolitical risks and rising inflation. Here's what Indian investors and borrowers need to know.

The RBI’s Monetary Policy Committee has just wrapped up its June 2026 meeting — and for investors, borrowers, and savers, the decision is both a relief and a signal to stay watchful.

In a unanimous vote, the MPC held the policy repo rate steady at 5.25% — but the tone of the meeting was anything but relaxed. Here’s what happened, why it matters, and what you should be thinking about for your portfolio.

The Decision at a Glance

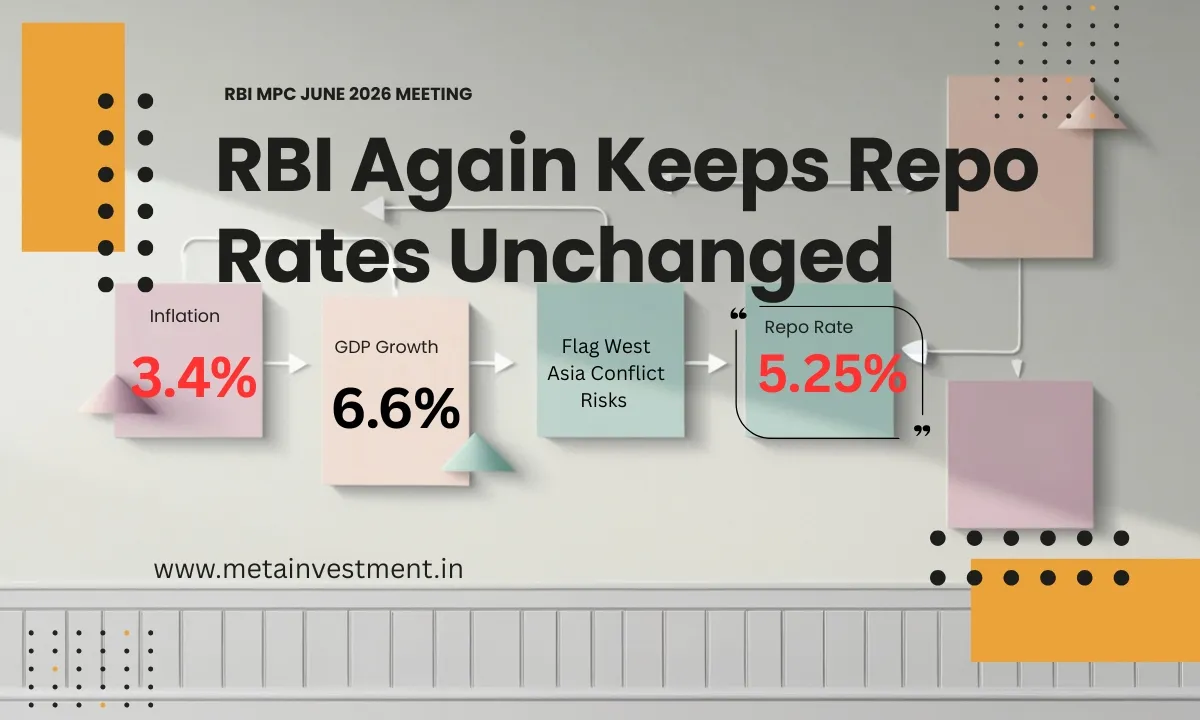

The 61st meeting of the Monetary Policy Committee, chaired by RBI Governor Shri Sanjay Malhotra, concluded on June 5, 2026 with a unanimous decision to keep the repo rate unchanged at 5.25%.

| Rate | Current Level |

|---|---|

| Policy Repo Rate | 5.25% |

| Standing Deposit Facility (SDF) | 5.00% |

| Marginal Standing Facility (MSF) / Bank Rate | 5.50% |

The MPC also retained its neutral stance — meaning it hasn’t committed to either cutting or hiking rates in the near future. It is watching the data closely.

This pause comes after a cumulative 125 basis points of rate cuts since early 2025. The RBI is now in a “wait and watch” mode as the global and domestic picture gets more complicated.

Why Did the RBI Press Pause?

The Global Storm: West Asia Conflict

The dominant theme of the June 2026 MPC statement is the ongoing West Asia conflict, which continues without any meaningful resolution. The consequences for India are real and mounting:

- Energy prices: Crude oil (Indian basket) averaged around $110/barrel during April–May 2026. Petrol and diesel prices were hiked by 7.4% and 8.4% respectively in May, adding an estimated 36 basis points directly to CPI inflation.

- Supply chain disruption: Freight and insurance costs remain elevated, squeezing merchandise exporters and pushing up input costs for domestic industries.

- Global monetary shift: Major advanced economy central banks are pivoting toward tightening — adding pressure on emerging market currencies and capital flows.

Inflation: Still in Range, But Rising

Here’s the picture the RBI painted on inflation:

- CPI inflation was 3.4% in March and 3.5% in April 2026 — still below the 4% target.

- But WPI inflation jumped to 8.3% in April (from 3.9% in March), signalling that input cost pressures are building in the pipeline.

- Core inflation (excluding food and fuel) held at 3.7%, but the RBI expects this to rise as businesses pass on higher costs.

Full year CPI inflation projection for 2026-27: 5.1%, with Q3 expected to be the hardest quarter at 5.9% — approaching the upper tolerance band of 6%.

The Monsoon Wild Card

The IMD’s forecast for the southwest monsoon is 90% of long-period average — classified as deficient. El Niño conditions are also likely to develop. A weak monsoon means:

- Higher food prices (food inflation was already edging up)

- Pressure on rural demand and agricultural incomes

- Greater uncertainty in the overall inflation trajectory

Given all this, the MPC felt it would be prudent to wait for greater clarity before making any rate move. A hike was not ruled out — it’s now firmly on the table if inflation generalises further.

Growth: Resilient, But Headwinds Are Visible

India’s economy showed impressive strength in 2025-26. Real GDP grew at 7.6%, supported by strong private consumption and investment. Manufacturing grew 13.3% and services 9.1% in Q3:2025-26.

For 2026-27, the RBI has projected GDP growth at 6.6%, reflecting a measured slowdown due to the global headwinds.

| Quarter | GDP Growth Projection |

|---|---|

| Q1 2026-27 | 6.6% |

| Q2 2026-27 | 6.3% |

| Q3 2026-27 | 6.5% |

| Q4 2026-27 | 6.8% |

What’s holding up growth:

- Domestic consumption remains resilient; two-wheeler and tractor sales posted double-digit growth

- Services sector PMI rose to 59.8 in May, driven by freight, digital, e-commerce and IT demand

- Manufacturing PMI at 55.0 in May — comfortably in expansion territory

- Government capital expenditure budgeted to grow 11.5% in 2026-27

- Bank credit grew 16.2% year-on-year as of May 2026

What could drag growth:

- Rising energy and input costs squeezing margins

- Sub-normal monsoon affecting agricultural output and rural demand

- Weak global demand and high logistics costs for merchandise exports

- Possible hardening of interest rates globally affecting capital flows

What This Means for Your Investments

🏠 Home Loans & EMI Borrowers

No rate change means no immediate change in your floating rate EMIs. But the risk of a future hike is real. Borrowers may wish to review their loan structure with their lender or financial adviser in light of evolving interest-rate expectations. Don’t assume cuts are coming anytime soon.

💰 Fixed Deposits

FD rates across banks have been softening in line with the earlier rate cuts. With inflation projected to rise toward 5.1–5.9%, locking into long-tenure FDs at current rates means your real returns (FD rate minus inflation) may be thin or even negative in the near term. Investors may evaluate deposit tenures based on their liquidity needs, interest-rate expectations and overall financial objectives.

📊 Debt Mutual Funds

This is where investors need to think carefully:

- Short-duration and corporate bond funds: Relatively well-positioned. Short-end rates are stable and credit conditions in the banking system are healthy.

- Long-duration funds and gilt funds: Generally more sensitive to changes in interest rates and may experience higher NAV volatility when yields rise. If inflation continues to rise and forces the RBI into a hike (possible in August or October), NAVs of long-duration funds will fall as yields harden. G-sec yields already firmed up in May after easing in April.

- Liquid and overnight funds: Safe harbour for parking money in the near term.

The suitability of short-, medium- or long-duration debt funds depends on an investor’s risk profile, investment horizon and return expectations.

📈 Equity Markets

The RBI’s growth projection of 6.6% for 2026-27 is a reasonable base, and domestic demand remains solid. However, equities are not without risk:

- Rising input costs could pressure corporate margins, especially in energy-intensive sectors

- A deficient monsoon could dampen rural consumption and FMCG/auto sectors

- Global FPI flows have been negative — net outflows of $13.7 billion so far in 2026-27 (up to June 2)

That said, the long-term India growth story remains intact. Investors with long-term investment horizons may consider evaluating diversified equity fund categories in consultation with their financial adviser, based on their risk profile and financial goals. Avoid making reactive decisions based on near-term macro noise.

Positive Signals for NRIs and Foreign Investors

The RBI used this policy meeting to announce several measures to attract foreign capital — relevant if you are an NRI investor:

- Expanded equity investment limits for NRIs, OCIs, and all Persons Resident Outside India (PROIs) in listed equity instruments without requiring SEBI registration

- Inclusion of 15, 30, and 40-year G-secs under the Fully Accessible Route (FAR) for FPI investment

- Concessional forex swap facility for ECBs by PSUs, and support for banks raising FCNR(B) deposits — both aimed at bolstering forex inflows

India’s forex reserves stand at a healthy $682.3 billion (as of May 29, 2026), covering about 11 months of imports — a strong buffer against external shocks.

Key Takeaways for Investors

- Repo rate stays at 5.25% — no immediate change in loan EMIs or FD rates

- Inflation is the bigger concern now — projected to touch 5.9% in Q3:2026-27

- Fuel price hikes and input cost pressures are working their way through the system

- A rate hike is now a possibility — the MPC is data-dependent and watching closely

- Debt fund strategy: Favour short to medium duration; avoid chasing long-duration gains

- Equity investors: Stay invested for the long term; avoid panic over near-term volatility

- NRI investors: New liberalisation measures offer expanded access to Indian capital markets

Looking Ahead: The Next MPC Meeting

The next MPC meeting is scheduled for August 3–5, 2026. By then, we will have more clarity on:

- Whether the monsoon deficit deepens further

- How much inflation has risen with the fuel price pass-through

- Whether advanced economy central banks have begun hiking and the impact on global capital flows

If inflation data in June and July surprises on the upside, a rate hike in August cannot be ruled out. That would be the first hike in this cycle, reversing some of the 125 basis points cut since early 2025.

Stay informed, stay diversified, and resist making knee-jerk changes to your portfolio based on any single data point.

Interested in Investing? Connect with Meta Investment

Meta Investment is a financial product distribution and services firm. If you'd like to explore whether a financial product is the right fit for your portfolio, our team will walk you through the details, help you assess suitability, and guide you through the onboarding process.

This post is based on the RBI Monetary Policy Statement (Press Release 2026-2027/385) and the Governor’s Statement (Press Release 2026-2027/386) dated June 5, 2026.

*Disclaimer:

This communication is intended solely for educational and informational purposes and should not be construed as investment advice, a recommendation, or a solicitation to buy or sell any financial product. Views expressed are based on publicly available information as of the date of publication and are subject to change.

The suitability of any investment category depends on an investor’s financial objectives, risk appetite, investment horizon and overall financial circumstances. Investors should consult their Mutual Fund Distributor, financial adviser or other qualified professional before making investment decisions.

Mutual Fund investments are subject to market risks. Please read all scheme-related documents carefully before investing. Past performance may or may not be sustained in the future and is not indicative of future results.*

Meta Investment – Your Investment and Insurance Companion.

Frequently Asked Questions

What did the RBI MPC decide in June 2026?

The Monetary Policy Committee (MPC) voted unanimously to keep the policy repo rate unchanged at 5.25% at its June 3–5, 2026 meeting. The MPC retained its neutral stance, citing uncertainty around the ongoing West Asia conflict, rising energy prices, and a sub-normal monsoon forecast.

What is the current repo rate in India after the June 2026 MPC meeting?

The repo rate remains at 5.25% as of June 2026. Consequently, the Standing Deposit Facility (SDF) rate is 5.00% and the Marginal Standing Facility (MSF) rate and Bank Rate are at 5.50%.

Why did the RBI keep the repo rate unchanged in June 2026?

The RBI chose to pause because while inflation is still within tolerance, risks are rising — fuel prices have been hiked, the south-west monsoon is forecast to be deficient, and global supply chain disruptions from the West Asia conflict are pushing input costs higher. The MPC preferred to wait for greater clarity before acting.

What is the RBI's inflation forecast for 2026-27?

The RBI projects CPI inflation at 5.1% for the full year 2026-27. It is expected to be 4.2% in Q1, rising to 5.1% in Q2, peaking at 5.9% in Q3, and then easing to 5.4% in Q4.

What is the RBI's GDP growth forecast for 2026-27?

Real GDP growth for 2026-27 is projected at 6.6%, with quarterly estimates of 6.6% (Q1), 6.3% (Q2), 6.5% (Q3), and 6.8% (Q4). India's 2025-26 GDP growth came in at 7.6% according to NSO's second advance estimates.

How does the RBI rate pause affect home loan and EMI borrowers?

With the repo rate unchanged, floating rate home loans and other retail loans will not see any immediate change in EMIs. However, borrowers should watch out — if inflationary pressures force a rate hike in the August or subsequent MPC meetings, EMIs on floating rate loans could rise.

What is the impact of the June 2026 MPC decision on debt mutual funds?

A rate pause in a neutral-to-cautious environment suggests limited upside for long-duration debt funds in the near term. Short to medium duration debt funds and corporate bond funds may be relatively better positioned. If inflation spikes further, rates could go up, which would hurt long-duration fund NAVs.

What is the RBI's stance in June 2026 and what does 'neutral stance' mean?

The MPC retained a 'neutral stance', meaning it is neither committed to cutting nor hiking rates in the near term — it is data-dependent and could go either way depending on how inflation and growth evolve. This is different from an 'accommodative stance' (rate cuts likely) or a 'withdrawal of accommodation' stance (rate hikes likely).

What risks does the RBI see for the Indian economy in 2026-27?

Key risks include: prolonged West Asia conflict disrupting global supply chains and energy prices; a sub-normal south-west monsoon and El Niño conditions affecting food inflation and agriculture; second-round inflationary effects from higher input costs; and weak global demand weighing on merchandise exports.

Is it a good time to invest in fixed deposits given the rate pause?

With rates on hold and inflation projected to rise, locking into long-term FDs may not be ideal as real returns (FD rate minus inflation) may compress. Short to medium-term FDs or floating rate instruments can offer more flexibility. Consult a financial advisor before deciding.

What happened to fuel prices before the June 2026 MPC meeting?

Petrol and diesel prices were cumulatively increased by 7.4% and 8.4% respectively in May 2026. This is expected to directly add about 36 basis points to headline CPI inflation, with additional second-round effects through higher input costs for businesses.

What new measures did the RBI announce for NRIs and foreign investors?

The RBI announced expanded investment limits for NRIs and Overseas Citizens of India (OCIs) in equity instruments. It also extended this facility to all Persons Resident Outside India (PROIs) at par with NRIs and OCIs. New G-sec issuances of 15, 30, and 40-year tenors were included under the Fully Accessible Route (FAR) for FPIs.

0

Join WhatsApp/Telegram/Arattai Channel

Join our channels for exclusive investment, finance, and insurance updates, fun content, and more.Read more about

- Financial Planning Checklist for Indian IT Employees Facing the 2026 Hiring Slowdown

- Master Your Financial Future with Our Expert-Led Webinars

- महागाईचा कूपन दरांवर होणारा परिणाम: फिक्स्ड-इनकम गुंतवणूकदारांचे मार्गदर्शक

- Liquid Mutual Funds: A Simple Guide for Indian Investors

- Mutual Funds in India 2026: How They Work, Types, SIP Returns & Selection Guide

- Portfolio Management Services (PMS) in India | Guide for HNIs & NRIs

- Best Tax Saving Options in India for 2025 | Section 80C & More

")